|

By Elliott Wave International As the world's leading stock markets continue to play stomach-hockey with investors via one triple-digit turn after another, the mainstream community takes solace in this core belief: No matter how uncertain things become, the Federal Reserve can at any moment swoop in to set the economy right. In reality — the… Read more The Federal Reserve Does NOT Control the Market |

Month: May 2010

Signs of Deflation You Might Not be Able to See Clearly

|

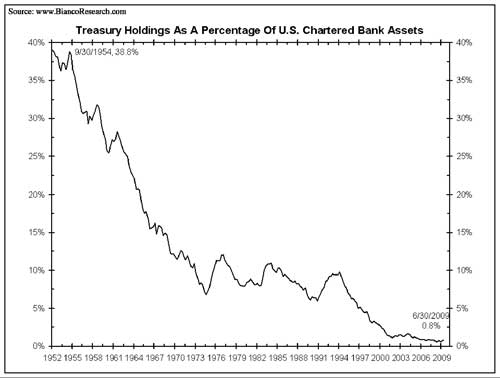

By Editorial Staff, Elliott Wave International The following market analysis is courtesy of Bob Prechter's Elliott Wave International. Elliott Wave International is currently offering Bob's recent Elliott Wave Theorist, free. Continuing—and Looming—Deflationary Forces The Fed and the government quite effectively advertise their efforts to inflate the supply of money and credit. But deflationary forces, to… Read more Signs of Deflation You Might Not be Able to See Clearly |

What Do These 8 Technical Indicators Mean for the Markets?

|

Editor's Note: The following article is excerpted from Robert Prechter's April 2010 issue of the Elliott Wave Theorist. For a limited time, you can visit Elliott Wave International to download the full 10-page issue, free. By Robert Prechter, CMT Technical Indicators It is rare to have technical indicators all lined up on one side of… Read more What Do These 8 Technical Indicators Mean for the Markets? |