What You Can Learn from Europe’s “Dow Theory”-esque Non-confirmation

By Brian Whitmer | European Financial Forecast editor

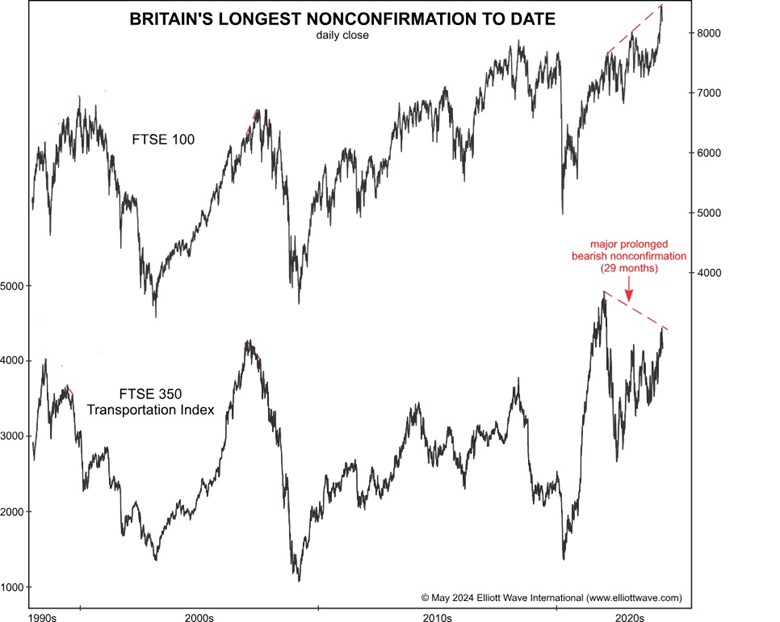

Charles Dow (yes, the one with the averages named after him) developed a foundational concept in technical analysis that requires that price movement in industrial stocks and transportation shares confirm one another.

The main condition for a Dow Theory non-confirmation occurs when one sector makes a new extreme absent the other. Its classic application is observing the position of the Dow Jones Industrial Average, an index of 30 “industrial” stocks, versus the position of the Dow Jones Transportation Average, an index of 20 “transportation” stocks. In essence, whenever one index fails to keep up with the other, in either direction, it suggests an impending reversal.

These concepts can be applied universally.

For example, right now over in Britain, the FTSE 100’s divergence with the FTSE 350 Transportation Index just pushed to 29 months.

This is a far more prolonged Dow Theory non-confirmation than that seen in July 2007 (seven months) or December 1999 (17 months). In 1999, the FTSE 100 eventually collapsed 53%, while the FTSE 350 Transports fell 66%. In 2007, the resulting declines were 49% and 77%, respectively.

In our view, Britain’s prolonged non-confirmation makes sense given a host of investor psychology and other extremes we’ve been tracking, not just in Europe but around the globe. If you want to stay up-to-date on our findings regarding the position of stocks and bond markets, currencies and the broad economic trends, check out some of our free must-read issues on www.elliottwave.com.